Strategic procurement in manufacturing shifts the focus from short-term cost savings to creating a lasting competitive edge.

Modern procurement teams need to understand global supplier networks, new manufacturing processes, and the impact of production relocations. And, as you probably guessed, cost is a big part of the equation here.

To make smarter decisions, you need transparent product costs, benchmarks, and clear savings opportunities. By collaborating with suppliers to identify cost targets, you set yourself up for success.

We've outlined 11 actionable best practices to help you turn procurement into a powerful tool for growth.

Contents

- Use demand forecasting

- Centralize your data to kick off supplier selection faster

- Define achievable and competitive cost targets

- Look beyond the price tag

- Master negotiations and contracts

- Build strong supplier relationships and manage risks

- Evaluate alternative manufacturing processes

- Set clear standards for costing methods

- Automate cost engineering and keep everyone in the loop

- Ensure suppliers deliver on their promises

- Evaluate supplier sustainability

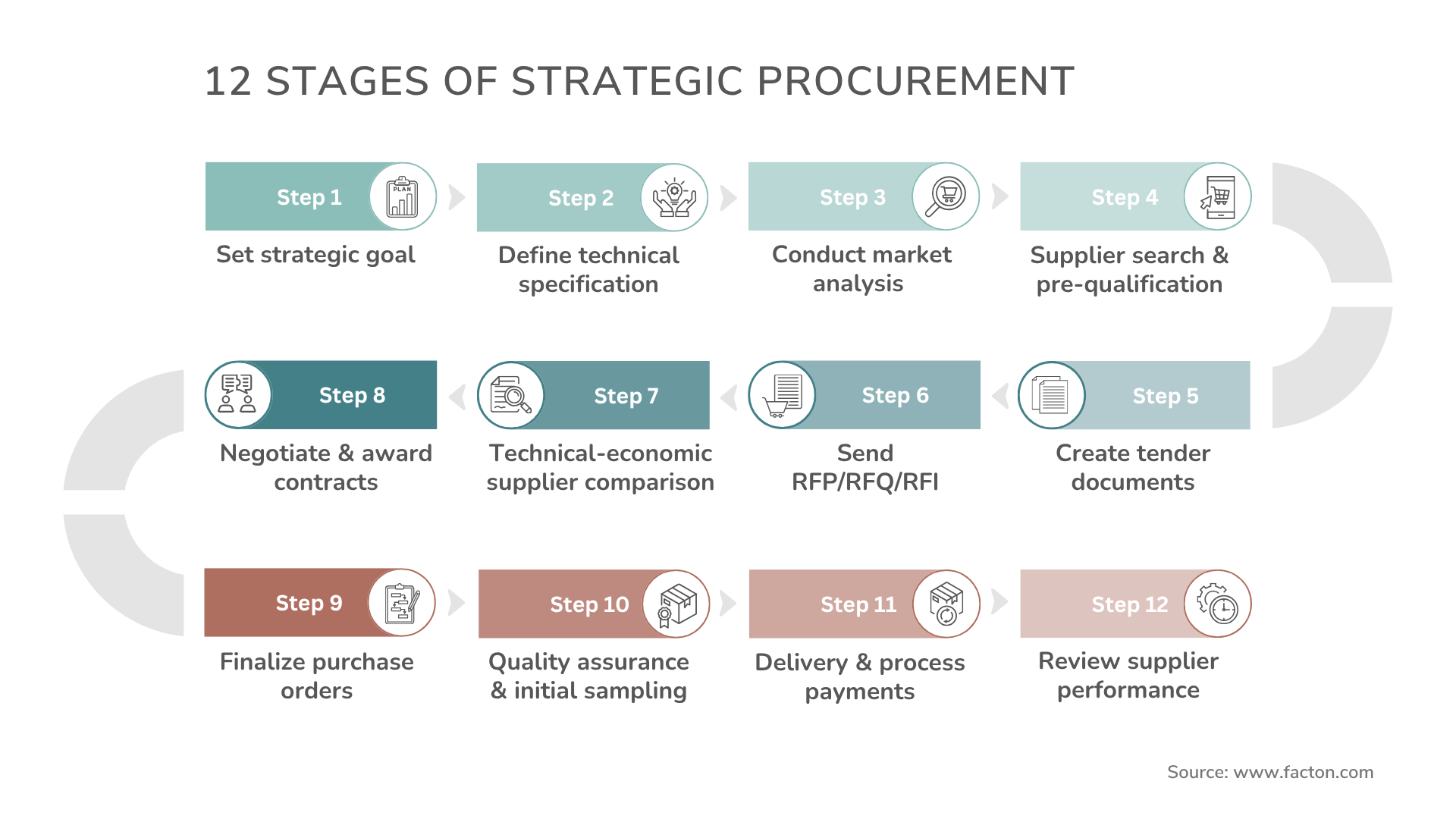

Here is how to stay on course through every stage of the strategic procurement process in manufacturing.

1. Use demand forecasting

Demand forecasting is integral to strategic procurement. It helps you plan production, manage inventory, and allocate resources more effectively to meet customer needs without overproducing and incurring unnecessary costs.

By using data-driven forecasting tools powered by advanced analytics and machine learning, you can account for real-time purchase trends, social media buzz, weather, inflation, and supply chain updates.

These tools quickly process massive amounts of data from in-house, third-party, and public sources to clearly show how demand might evolve.

2. Centralize your data to kick off supplier selection faster

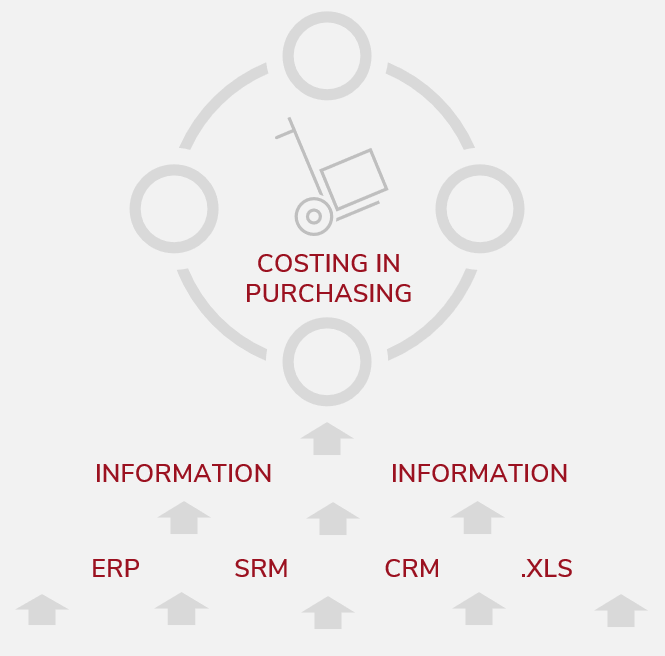

When a new component request comes in from product development, the supplier selection process starts with critical questions: Are these products already on the market? Which suppliers have designed something similar? What were the previous costs, and how do we calculate the new ones?  In strategic procurement, the challenge lies in quickly finding accurate, relevant data to answer these questions. And you should have that part figured out ahead of time. Once those component requests start rolling in, sifting through old folders and chasing down departments for missing information becomes a massive time drain.

In strategic procurement, the challenge lies in quickly finding accurate, relevant data to answer these questions. And you should have that part figured out ahead of time. Once those component requests start rolling in, sifting through old folders and chasing down departments for missing information becomes a massive time drain.

Save yourself the trouble and centralize your data in one searchable platform instead. It's faster, simpler, and provides the reliable information you need to make decisions and keep things moving.

3. Define achievable and competitive cost targets

Different approaches, such as top-down or bottom-up calculations, can be used for target costing.

- Top-down costing helps you set ambitious yet achievable goals from the start, providing all departments with a clear direction to follow. It uses benchmark data to ensure your products are developed within a financially sustainable framework. By aligning teams around these top-down targets, you build a solid foundation for success that balances ambition with practicality.

- Bottom-up costing uses the parameters you already know to estimate the costs of assemblies and components. This approach helps you pinpoint where you have wiggle room to make production efficient and profitable.

While both methods differ, they need one thing to be effective—up-to-date, accurate data that reflects real-world supplier conditions.

This is especially crucial in areas prone to change, like material prices, wages, or machine investments. By staying on top of these shifts, purchasing teams can ensure their target costs remain realistic and aligned with current market conditions.

Depending on the industry, procurement and cost engineering contribute between 60% and 85% of a product's added value. So, get procurement involved early and equip them with the proper methods and calculation capacities. The sooner they're in the loop, the better your chances of hitting those shared goals.

4. Look beyond the price tag

When shortlisting suppliers, keep in mind that finding the ideal strategic sourcing partner requires more than low costs. You need a partner who truly understands the complexity of your products, meets your specs and tolerances, and delivers consistently on time.

Look for suppliers with solid quality management systems, certifications, and a commitment to your ESG goals. Cost is closely tied to quality and delivery time. Think of it as balancing QCD—Quality, Cost, and Delivery. If a price seems way off (too high or too low), dig deeper to understand why and see if it aligns with your expectations. Do your homework: run financial checks, talk to references, visit their site, and test samples to ensure their claims stack up. A little extra effort upfront can save you headaches down the road.

5. Master negotiations and contracts

Once you know your target costs and have a pool of potential suppliers, it's time to explore pricing, payment terms, and service-level agreements. Contract negotiations are arguably the most crucial step in the strategic procurement workflow. Think of it as a balancing act: You want cost savings, but you also want a supplier who feels valued and motivated to deliver.

Explore options like volume discounts, long-term contracts, or performance-based incentives to find common ground. And don't underestimate the power of a solid, clear contract—it sets expectations, reduces risks, and keeps disputes at bay.

Maintain open communication and review contract terms regularly. That little effort keeps everyone on the same page and helps drive continuous improvement.

6. Build strong supplier relationships and manage risks

Focus on collaboration to establish stronger partnerships with your key suppliers. Open communication is key—share information, solve problems together, and plan ahead for disruptions such as supply chain issues or price fluctuations. Consider establishing supplier development programs to support your partners' growth and alignment with your evolving needs.

Don't put all your eggs in one basket—reduce risk by diversifying suppliers and locking in raw material prices with hedging contracts. Maintain a buffer stock of critical materials on hand and always have a backup plan in place. Containment plans are a must, whether it's a natural disaster, a political crisis, or another global pandemic.

7. Evaluate alternative manufacturing processes.

When cutting costs through strategic procurement, exploring alternative manufacturing processes can make all the difference.

Start by using precise cost models that give you realistic estimates of manufacturing times.

These models factor in the latest developments in manufacturing technology and help you compare options—even if you don't have the specific technology or expertise in-house.

This equips your purchasing team to have smarter, more productive conversations with suppliers. Together, you can develop solutions that slash costs and optimize investments throughout a product's life cycle.

8. Set clear standards for costing methods

To make smart decisions in planning or production, you need a reliable way to compare scenarios and suppliers.

Start by standardizing your costing methods across the board. This ensures every estimate—regardless of who creates it, when or where it's created, or which supplier is being evaluated—is consistent, accurate, and easily reproducible.

Without clear standards, comparisons become irrelevant, and you risk missing real opportunities for cost savings. By adopting a company-wide approach to costing, you'll make better, data-backed decisions and uncover areas to cut costs effectively.

9. Automate cost engineering and keep everyone in the loop

Cost engineering plays a massive role in strategic procurement. However, it can be quite challenging as multiple stakeholders—suppliers, R&D teams, and purchasing departments—need clear, real-time cost updates and optimization plans. So, how do you keep everyone on the same page without wasting hours on manual updates? This is where automation kicks in.

With the right tools, you can send calculations instantly in one click, ensuring all teams stay informed about cost developments. Integrating variant management adds even more clarity, giving everyone a shared view of cost developments.

With numerous stakeholders, communication matters as much as the data itself. Tailor how you share updates with platforms like Tableau or Power BI. Personalized dashboards and cross-functional reports make it easy to track progress and address concerns early, helping teams align faster.

To get the best results in Should Costing, focus on global teamwork and give your teams the tools to succeed.

10. Ensure suppliers deliver on their promises

Suppliers may shine during negotiations, but how do you know they meet their commitments once the contract is signed? Without the right tools and processes, tracking their performance is nearly impossible, which can lead to big problems such as unexpected quality issues, delays, or rising costs.

Stay ahead by using measurable metrics. Automotive manufacturers refer to the Supplier Quality Score (SQS). The SQS evaluates suppliers based on delivery performance, service quality, and price. It's calculated by multiplying the number of parts delivered on time by their quality grade, then dividing by the total number of parts. Aim for an SQS of at least 80% to ensure suppliers consistently meet your standards.

You can also monitor compliance with specifications during quality inspections and audits.

11. Evaluate supplier sustainability

Manufacturers face a big challenge when it comes to sustainability, and most of the impact lies in their supply chains.

Did you know your supply chain emissions (Scope 3) can be over 20 times higher than those of your direct business operations (Scope 1 and 2)? Add in issues like ethical sourcing, water use, and labor practices, and it's clear why engaging suppliers is critical.

Ensure suppliers stay committed to sustainability—measuring how well they follow responsible environmental and social practices. Consider metrics such as greenhouse gas emissions, ethical sourcing audits, water reuse, and certifications like ISO 14001.

Work closely with your suppliers, share your goals, and show them how they can help reduce emissions and build more resilient supply chains. Yes, it's a challenge—54% of manufacturers say limited control over suppliers is their biggest hurdle—but it's also an opportunity to protect your brand, meet regulations, and make a real impact.

About FACTON:

FACTON was founded in 1998 and stands for outstanding expertise in enterprise product costing. Since 2020, the company has been part of Constellation Software Inc., Canada's largest software group. With teams in Germany and North America, FACTON serves a global customer portfolio, including Auria Solutions, Mahle, Fresenius Medical Care, MANN+HUMMEL, Vibracoustic, Porsche, and other well-known OEMs.